Section 12J (of the Income Tax Act) is an incentive granted by SARS to encourage investment into South African SME’s which gives investors into section 12J funds the ability to write off 100% of their investment against their taxable income in the year they invest.

Individuals, companies or trusts with large PAYE or provisional tax bills that are looking for tax-efficient investment options. These taxes are due on income earned from:

Salaries or bonuses from employment

Property rentals or interest income

Capital gains from the sale of properties, businesses or shares

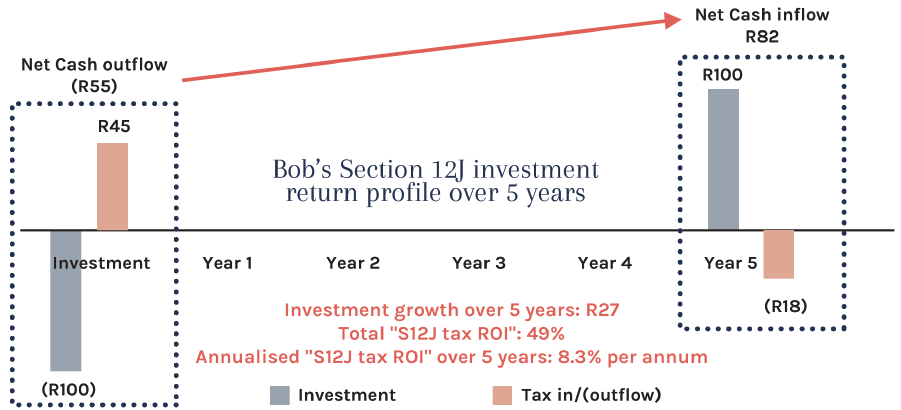

Bob invests R 100 into a Section 12J Fund. The investment generates no returns and he merely receives his capital back (R 100) in 5 years time. This graph illustrates the resultant cashflows (net of tax) over the investment term. Bob has a 45% marginal tax rate and an effective 18% CGT rate over the 5 years.

Yearly investment contributions are limited to R2.5 million for individuals and trusts and R 5 million for companies

Investment holding period is at least 5 years

Investment minimums are at least R 100 000 per investor per fund

Capital gains tax payable on exit, even if no actual gain was made